The setup

The "Bitcoin Strategic Reserve" (BSR) topic has popped up in many places lately, following its first appearance in the US more than a year ago. To my satisfaction, it surfaced recently in the public debate sphere in Luxembourg.

With OffChain Luxembourg a.s.b.l., we had launched at the beginning of 2025 "The Orange Heart Initiative", a public call to politicians, business leaders and the general electorate to seize upon and debate the topic.

In the red corner ...

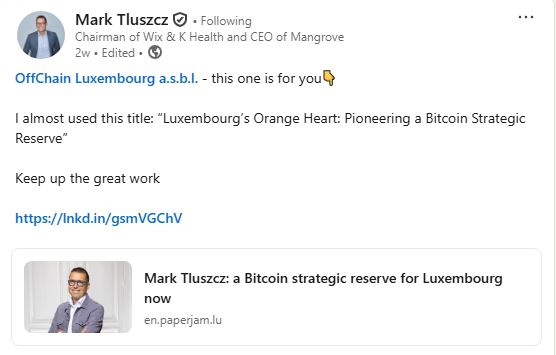

Things started moving when a prominent business figure, Mark Tluszcz, wrote a public tribune arguing in favor of a BSR for Luxembourg. Kindly referencing our initiative, Mark called his LinkedIn article "Luxembourg's orange heart".

The umpire ...

A highly influential MP and city alderman, Laurent Mosar then echoed Mark's article, asked the typical questions and laid out the standard concerns.

In the blue corner ...

The scene was set when a second well-known venture capitalist, Pascal Bouvier, replied to Mark Tluszcz taking the opposite view: a BSR would make no sense for Luxembourg. His approach and reasoning were mostly sound ... except that the author relied on what I felt were false, or at least debatable, assumptions.

They can't both be right, can they? ...

In this article I'll follow Pascal Bouvier's approach, for several reasons: Mark's argument for a BSR is primarily a call backed by a vision of the future. I, and everybody else in OffChain Luxembourg asbl, happen to share that vision, but if someone does not, it is hard to argue with a projection of things that might come to pass, but might also not happen. In contrast, Pascal's rebuttal is rational and based on comparison with visible "anchors" such as the "Strategic Petroleum Reserve" that several countries manage (the US, China, Japan, India).

As Pascal rightly says, a strategic reserve exists to insure resilience in case of disruption due to crises, wars, economic disruptions, embargoes, natural disasters. What he doesn't see though, is what type of disruption could a BSR protect against?

The crisis scenario

If and when Mark (or anyone else) will debate Pascal, I trust he should come up with concrete, down-to-earth arguments facing and refuting the skeptics worries, rather than with a projection of the future where a BSR would burnish Luxembourg's image as an advanced fintech hub and attract talents - however right and compelling that vision is. He should, I believe, lay out one or more possible crisis scenarios (the more plausible, the better) in which Bitcoin could prove vital to the continuation of economic activities.

Unfortunately, such a crisis scenario is not difficult to imagine, and it becomes ever more likely every day. At the heart of it, the current international trade system and the monetary infrastructure underpinning it. The signs of an impending global crisis have been clearly seen by many observers. I've chosen to illustrate here with yet another LinkedIn article from widely respected Professor Bruno Colmant. I posit that Pascal Bouvier knows and respects his opinion too, but I want to emphasize that Prof. Colmant is far from alone in warning about Trump's tendency to weaponize the US Dollar's dominance in international trade: Alicia Garcia Herrero, Senior Research Fellow at Brussels-based "Bruegel" think-tank and Maurice Obstfeld from the Peterson Institute for International Economics have also sounded the alarm to various extents.

Prof. Bruno Colmant argues that an unsustainable US public debt burden and a dangerously fragile dollar are setting up the world for a rude awakening. This article is just one piece in a broader view that paints a much darker picture. Bruno Colmant has written several such pieces alerting about the possible monetary disruption that seems to lie in front of us. In a subsequent post, Prof. Colmant looks closer at the nascent embrace between crypto and traditional finance and notices that with the GENIUS act, the US has ignited a stealth monetary war.

It is important to consider that, in some commentators' view, the world is currently at war, albeit a "monetary" and "stealth" one ... Unlike a conventional war, a monetary war does not deplete stocks of shells or ammunition, a monetary war depletes trust. When talking about the Trump regime, which destroyed or severely damaged the trust earned through decades of good faith cooperation in the first three months of his presidency, Prof. Colmant talks of "digital fascism".

Unlike classical wars, monetary wars do not deplete stocks of shells or ammunition. Instead, monetary wars deplete mutual trust.

The whole geopolitical post-WW2 order is collapsing under our eyes. China is shrewdly propping up Russia in order to keep the US busy so it cannot fully pivot towards the Chinese sphere of influence. Now imagine that Xi Jinping decides to invade Taiwan. This is the kind of global crisis every country should be prepared for. Think of the consequences on the vast network of international trade that is today oiled by the US Dollar.

An open confrontation between China and the US will likely force other countries to take sides. Europe is understandably expected to side with the US. But imagine for a second that Brazil, for instance, or Indonesia, make a sovereign decision to side with China. The EU imports iron ore and oil for its industry, soy meal for its cattle farmers, coffee for its consumers, and many other products from Brazil. A majority of these exports were paid for in ... US Dollars. But if Brazil makes the sovereign decision to side with China, it will likely be "sanctioned" by the US and cut off from USD financial circuits. It will become impossible to pay Brazilian exports in USD. And while for some of those contracts the Brazilians are probably going to accept euros instead, the induced trade friction for the remaining part will be enormous.

Furthermore, Europe at least does have a credible currency that could grow in importance as an alternative to the USD. But let's think of other countries, such as Australia. In 2023 almost 90% of Australia's exports and almost 60% of its imports were invoiced in USD. In a world where the US and China will force countries to take sides, and those siding with China will likely lose access to the USD, you can imagine the difficulties that Australia, a staunch US ally, will face in its trade relationship not only with China (a big trading partner) but also with countries such as South Africa or Pakistan (likely China allies).

Some readers might be tempted to dismiss such scenarios as unlikely and mere "fear-mongering". I'd like to invite them to search their memories for the summer of 2007 and how, back then, all commentators were insisting that "house prices had never in the history of the US declined nationwide". They had never done it, until they did ...

I'd like to remind my readers that humans are notoriously bad at spotting sudden changes in advance. The human brain naturally assumes that the future will look, to a large extent, like the past.

What have international trade disruptions to do with Bitcoin?

Currently, very little. But Bitcoin is an algorithmic product and, despite some fluctuations induced by human behavior, its trend is abundantly clear. The argument that "Bitcoin is volatile" only makes sense in a stable world with stable fiat currencies and reliable financial rails. This is by-the-way one of the weaknesses of Pascal Bouvier's argument: he tends to approach Bitcoin not as a possible currency but rather as financial asset with a monetary value expressed in Central Bank (fiat) currencies.

But in a world in geo-political flux, the relative values of fiat currencies risk becoming unpredictable, making these currencies impractical for cross-border trade. For a country coming under US sanctions - and the erratic nature of the current US president tends to indicate that nobody is safe, not even Denmark, given Trump's craving for Greenland - the value of the USD for those countries will suddenly collapse to near zero, because the Trump administration might "freeze", sanction and generally censor their USD holdings. Consequently, the value of Bitcoin, a censorship resistant representation of value, will increase many-fold for those countries.

Imagining that under such a stressful international situation, alongside the use of local currencies such as BRL, AUD or ZAR, a significant portion of bilateral trade contracts could be settled in Bitcoin instead is not that difficult.

Bitcoin offers fast, robust, independent settlement rails that can withstand American interference. For Bitcoin to become a settlement vector for trade in goods all that's needed is a "on / off toggle" of one country accepting it - once that dam cracks, the trickle can rapidly turn into a flood, as is the nature of confidence plays. And currencies are precisely that: "partially trusting" a currency is not a stable situation - you either trust it or you don't.

The fact that nobody has yet trusted Bitcoin in international trade is therefore an unreliable indicator of whether it may happen in the future. And this is perhaps the most valuable characteristic of Bitcoin: by design, it intrinsically is trustworthy.

To sum up the line of argument until now, Bitcoin, an independent financial circuit that nobody owns, could prove salutary for the continuity of international trade in a world torn between two opposing camps, one of which owns today's currency of international trade.

Bitcoin is highly liquid: it is immediately accessible and can be mobilized in seconds and change hands in under one hour with full reliability even under situations of systemic or geopolitical disruptions. Indeed, despite its considerable influence, the US can not cut off a country from the internet (nor cut out its electricity supply). Sending Bitcoin only requires internet access and the amount sent is almost the same as the amount received, with barely any friction and very low transaction costs.

Bitcoin is not accepted yet as a currency, but as I pointed out above, this is no indication that it won't become suddenly an acceptable alternative, because this is the nature of trust objects: they are binary - once enough countries begin using and trusting Bitcoin, the movement becomes self-reinforcing and, before you know it, everybody is using and trusting Bitcoin.

By design, Bitcoin, an algorithmic product, is intrinsically trustworthy. The fact that it hasn't been trusted yet in international trade is not a reliable indicator of it becoming trusted in the future, as currencies are "binary trust objects": once enough countries begin using it, the movement becomes self-reinforcing.

Pascal Bouvier likens Bitcoin to Pokémon cards and some of his readers like that analogy. While amusing, it is a deeply flawed analogy : Pokémon cards are under the control of one entity, "The Pokémon Company"; nobody can object to the owner of the Pokémon franchise printing and selling more cards, thus diluting the rarity value of the existing ones. Inventing new cards or cancelling existing cards and generally doing whatever it pleases with the franchise it owns. Because of that, since 1998 when Nintendo, Game Freak and Creatures Inc. established the joint controlling company, only a relatively stable proportion of people assign value to Pokémon cards. In contrast, over the past 15 years, as the number of people understanding the fundamental characteristics of Bitcoin has increased, that increase has been reflected in a steady overall increase in Bitcoin's price.

And that, despite the "Cambrian explosion" in the number of currencies inspired by Bitcoin, relying on similar or better technologies and offering better functionalities.

It is said that, unlike Pokémon cards, the governance of which is "centralized" in the hands of one entity, Bitcoin is "decentralized". What that means is that because of diffuse control, changing anything about Bitcoin is incredibly hard. This confers Bitcoin predictability, a paramount feature for a currency, and the underlying reason why Central Banks aim for price stability.

Pascal also mistakenly sees "liquidity" with respect to Bitcoin's conversion to fiat currencies. This is a glaring blind spot in his reasoning which challenges the soundness of his argument: the strategic importance of Bitcoin is not as an asset to be converted to a pivot fiat currency, but as an alternative currency standing on its own, challenging the Central Bank-issued currencies.

This aspect also weakens his fourth argument based around an alleged "operational fragility": Bitcoin does not depend on "exchanges", because as Pascal himself notes, the purpose is not to "play", "speculate" and "make fiat gains", but to use it as is, as a transferable unit of account and store of value. Anecdotally, the Mt.Gox exchange was processing about 80% of Bitcoin trades in 2014, at a time when Bitcoin was a lot more fragile than it is today; yet Bitcoin shrugged MtGox's sudden demise even back in 2014. Today Bitcoin is traded in hundreds if not thousands of exchanges all over the world, none of which can impact its price, volume or market behavior.

Nor does Bitcoin depend on "friendly jurisdictions", especially under the crisis scenario laid out above. A convincing illustration is the ban on Bitcoin mining that China suddenly enacted in 2021 (after having banned cryptocurrency transactions in 2018), at a time when almost two thirds of all hashing power was concentrated in China. Sometimes called "the honey badger of money", Bitcoin again shrugged. Mining rigs were exported to other places, like in a game of "whack-a-mole", and hashing power quickly recovered.

Furthermore, Bitcoin allows sovereign nations to resist the financial bullying and coercion of an unpredictable and untrustworthy US administration that might turn unfriendly (for instance because it wants Greenland or the Panama canal).

Yes, Bitcoin depends on electricity and on the internet - but don't all (bank) money transfers for the purpose of settling international trade depend on electricity and the internet? Let's then compare what's comparable.

Remains the question of pricing goods and services in Bitcoin under an unstable international monetary regime where the value of the USD itself is called into question. How much Bitcoin for a ton of iron ore? How much Bitcoin for a ton of Brazilian coffee? While hard to say in advance, these appear as questions best left to the markets to settle. If the global monetary system is in complete disarray and a new value scale will have to emerge, we will remember that we were in the past been able to price goods and effort in salt, sea shells or gold. Such is the effect of crises.

Therefore, Bitcoin is a strategic asset. Both its issuance and its transfer are independent of nation states. Bitcoin functioning is predictable and therefore trustworthy. In the not-unlikely scenario of an international monetary crisis, Bitcoin can alleviate the worlds' dependence on the US Dollar for international trade, which is a vital component of modern economies.

Revisiting Bitcoin

Pascal's second argument asks "what is bitcoin"?

Bitcoiners would answer this question by explaining the elegance of Satoshi's whitepaper and glossing about crypto-anarchism, b-money, hashcash, and timestamp servers. About the auditability of the open-source code and the unparalleled reliability of a network that has added a "block" to the "blockchain" every 10 minutes for the past 15 years without interruption.

In contrast, Pascal eludes completely the intrinsic nature of bitcoin as a technological product and instead misplaces his focus on ... Bitcoin's pricing by the markets in fiat currencies. He argues that Bitcoin is the archetype of a J.M. Keynes "beauty contest" asset, where prices are formed in an infinitely-reflexive guessing game of what everyone thinks the price will be.

The fatal flaw in Pascal reasoning is ... ignoring history, ignoring the technology, ignoring the Bitcoiners. Indeed there is little need for an object of Bitcoin's nature in a world where trust reigns and it is honored by its depositories.

Yet the Great Financial Crisis of 2007-2009 was a massive breach of trust that shocked the world to its core. Pascal has certainly lived it firsthand, but has probably forgotten it. For him and all those who need a reminder of history, I recommend re-watching the excellent 2015 movie, "The Big Short". It is at that very moment, and in response to those very events that Bitcoin was born.

When it was launched, Bitcoin was little more than a promise rooted in technology. Few people understood the power of that technology and started believing in it. Sixteen years on, that technology has been thoroughly proven. For all practical purposes, it is the most reliable IT system ever built by humans. As confidence in it increased, its price followed and the price increase attracted a lot of people seeking fiat gains. Most of these followers that have begun appearing once Bitcoin began trading in earnest in the middle of 2011 are indeed fickle. They mainly focus on what other think the price of Bitcoin will be in the future, typical of J.M. Keynes description of the "beauty contest".

Although far less numerous, those who are the bedrock of Bitcoin's fiat value are the early Bitcoiners, those who spent time and resources "mining", securing, and expanding the network in the first 18 months of Bitcoin's existence. During that time, Bitcoin was not traded and had no monetary value, so they weren't doing it "for the (fiat) money". Although more than 12, they were comparable to Jesus's 12 apostles, acting out of faith. The early Bitcoiners break Pascal's narrative of the "beauty contest". They weren't in it for the money then